What to expect in the meantime: Commentary updates may be delayed, absent or irregular. Charts may display errors, broken links, or outdated formatting. Pages may shift without warning as we wire up the new infrastructure.

What hasn't changed: The wheat trend analysis and BoR status calls continue — same rigor, same pre-dawn commitment. If you need a specific chart or have questions, use the Contact page or use the green button labeled “get on update list and you will receive an alert when the final countdown to launch is immanent .

We're working at a furious pace to provide this rollout that we are very excited to offer our dedicated readership. Thank you for your patience — the new MarketBullets is worth the wait.

-Gabe

More Sense Per Bushel™

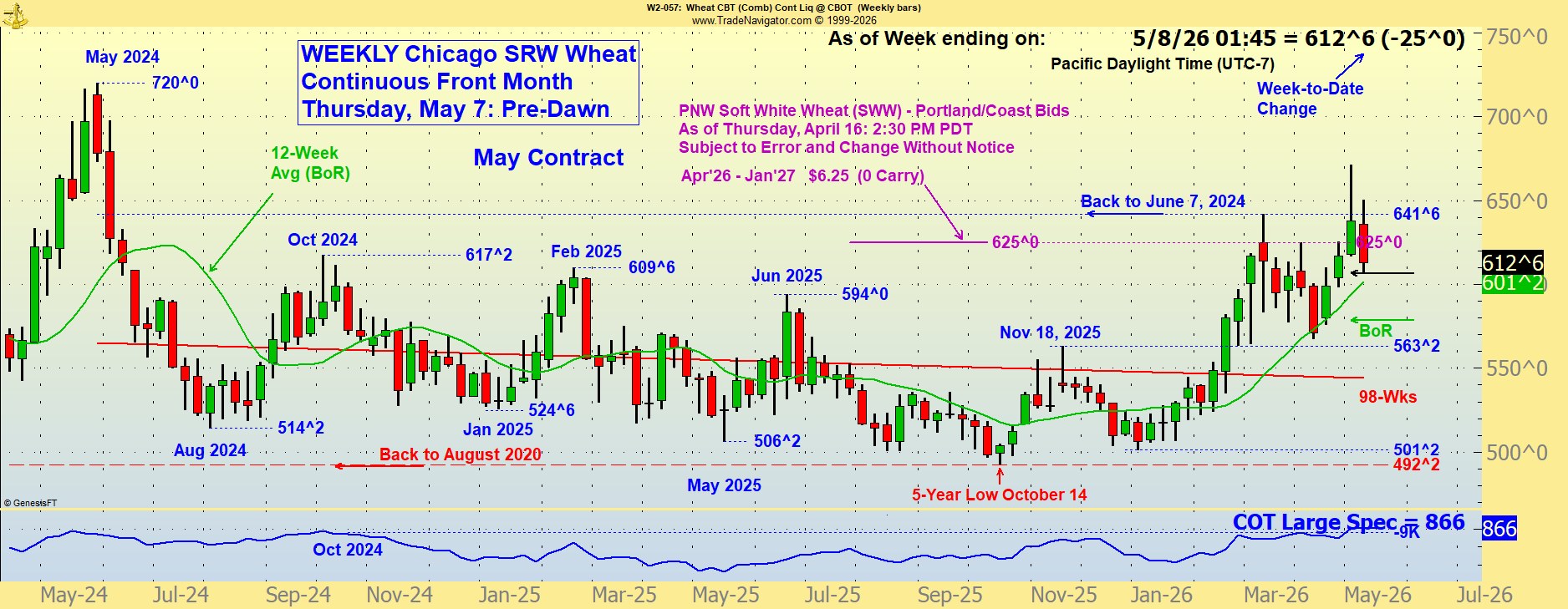

WEEKLY Chicago SRW

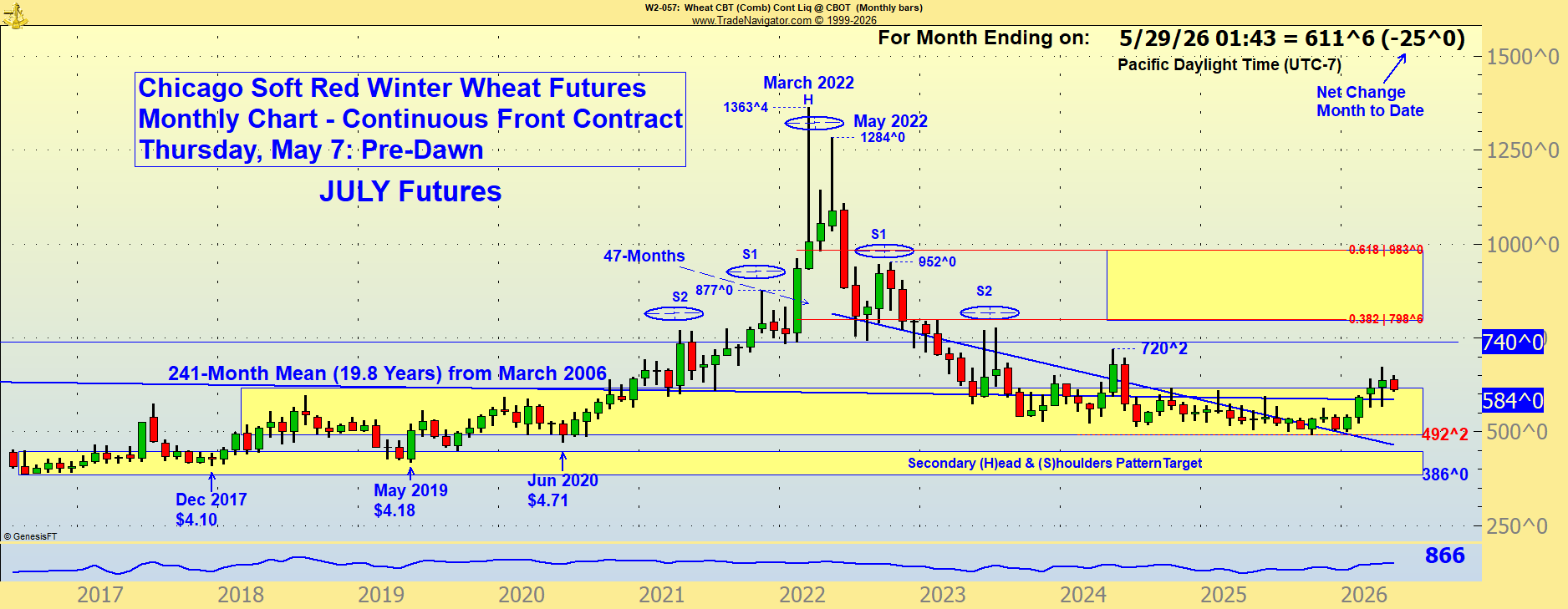

**Wheat Price Trends and Peripheral Markets; Charts and Commentary. More Sense Per Bushel.*

Sunday, July 26, 2026: 6:00 PM:

Iran offers suspension of attacks as long as U.S. halts strikes. Crude oil down $7.00 to 85/Bbl.

Wednesday, July 22, 2026: Pre-Dawn

Chicago Soft Red Winter (SRW) wheat has been trading at its best prices since June of 2024, driven there by hot temperatures in the northern hemisphere that cut short the maturation of a substantial amount of both winter and spring wheat, but the most powerful factor pushing wheat is a drastic reduction in Russian and Ukrainian wheat shipping during the heights of their respective harvest seasons The Sea of Azov, from which about a quarter of Russian wheat is moved each year, has been cut off by Ukraine’s long-range drone weapons across the Kerch Strait. Russia’s response has been to hit at Ukraine’s export facilities, reducing wheat flow from Black Sea origins even more. The response of the market has been enough to change the trend pattern to a positive slope and raise expectations.

Fuel costs had been easing until resumption of airstrikes on Iranian military infrastructure, as well as Iranian strikes on their neighbors. The Crude oil market has currently reached back up to the levels of mid-June, although those prices in the $80-$87 per barrel for West Texas Intermediate (WTI) are well below previous highs from $100 to $118 per barrel in February through April. Many observers expect the current phase to be limited in duration. The Iranian economy is under severe pressure, but the Straits of Hormuz are still effectively closed.

The trend for wheat is higher. The Box-O-Rox indicator is in Suspend Sales mode since July 10th. It will require at least a decline of 50 cents to switch back to “Execute Scheduled Sales”. Discussions about if/when to exit current positions without regard to BoR indications are underway.

There is a sense of relief in the air, but volatility will be a challenge ahead.

Stay tuned, as MarketBullets Daily Commentary is resuming very soon.

Wednesday, May 6, 2025: Pre-Dawn

Possible war ending - The market says yes (Crude oil down hard, wheat along with it).

Diesel dropping on crude oil decline.

Market looks like re-set is underway, with multiple intermediate trend changes.

Box-o-Rox has come down to “Exit Trigger” and may produce “Execute Suspended Sales” indication (only 1 tranche is suspended since May 1). Watch for close below the line on BoR page.

Friday, May 1, 2026: Close

· Europe (Euronext/MATIF): UK equity markets and UK commodities, including wheat, will be closed Fri. Many European exchanges are closed for the May Day holiday period, including Friday and Monday.

· China: The Zhengzhou Commodity Exchange (ZCE) will be closed from Friday, May 1, to Tuesday, May 5, 2026, for the Labor Day holiday.

· Other Regions: Labour Day is observed in several regions, including Ireland, parts of Australia, and some Caribbean nations, likely impacting local cash market activity.

· US Markets (CME Group and MIAX): Monday, May 4, is not a standard grain trading holiday, but the global market holidays often lead to reduced trading activity

The above conditions do not prevent wheat price movement, as low volume can make the market a bit more vulnerable to sudden changes, but normally it is a quiet session.

MarketBullets® Friday, March 27, 2026: Pre-Dawn

Wheat trend still upward - Box-o-Rox on “Suspend Incremental Sales” currently holding two (2) tranches of 8.33% of expected crop each. Another tranche will become active on April 1 unless the Chicago May contract is below the main BoR indicator line, which is currently at $5.68 (47 cents below current trade).

Front month West Texas Indermediate (WTI) Crude oil is trading at 93.79. Brent (North Sea) Crude oil is at about 100.82 last quoted.

Dollar Index up, now +2.30% Month-to-Date, as interest rates are rising.

Stay tuned. - Gary

MarketBullets® Wednesday, March 25, 2026: Pre-Dawn

Crude oil did not get above $93.36 in the nearby futures trade on Tuesday and in Wednesday early trading hours the May contract was trading between $86.59 and $89.57. Wheat remains coupled to crude oil, as without a recognizable ending to the war in Iran there is a continuation of market anxiety. The strongest hint of the wheat price effect of potential cessation of war was seen at 4:00 AM PDT Tuesday when the price of Chicago May futures dropped more than 20 cents in under 10 minutes due to President Trump’s de facto public announcement of “good” talks with Iran. The odds of an ending to the conflict seem to be low, but the consensus is still being expressed in terms of weeks.

The Chicago price as we type furiously away in the wee hours of Wednesday is below the Box-o-Rox exit trigger price for any increments that have been held back. The difference is large enough to make the status change to “Execute all previously suspended sales”. The ongoing status will remain “suspend” for any new incremental sales that are already on the calendar as long as the price remains above the longer (60-day) indicator line.

Meanwhile, the crop condition prospects of large portions of the Hard Red Winter (HRW) region in the U.S. continue to decline on lack of moisture as wheat emerges from dormancy. This underlying factor amounts to price support, and will eventually be the dominant driver of the spring season.

Wheat export inspections for the week ending March 19 totaled 458,411 metric tonnes (16.843 million bushels), up 33% from the last week but down 5.5% from the same week last year. 2025-26 to date, wheat shipments total 732.2 million bushels, up 18% from the same period in 2024-25.

It is unlikely that we will see large position adjustments among the funds in this environment unless there is another Truth Social banger. The market is still operating as the world awaits the next move in the Middle East.

Stay tuned in. The frequency of the Warm Signal will take some hunting, but it’s always there for us.

-Gary

MarketBullets® Tuesday, March 24, 2026: Pre-Dawn

1. THE TRUMP TRUTH SOCIAL REVERSAL — THE PRICE EVENT THAT DEFINES TODAY'S TRADE: As the Iran war enters its fourth week, President Donald Trump announced that the United States has engaged in diplomatic talks with Iran and is taking a five-day pause on strikes against Iranian power plants and energy infrastructure - Politico.Iran denied the talks and said Trump's move was designed to lower energy prices and "buy time" to implement his military plans - Barron's. The 5-day window expires Friday/Saturday — meaning this week's trade is essentially a countdown clock. The denial from Tehran is not bullish reassurance for oil-bound wheat price - Bloomberg.

2. “HEADLINE-TO-HEADLINE” TRADING IS THE MARKET'S NEW OPERATING SYSTEM: Headline-to-headline trading continues. As of March 23, 2026, the market finds itself caught between the reality of a "risk premium" driven by the blockade of a global chokepoint and the sobering math of a U.S. domestic wheat export machine that is losing its competitive momentum. The combined managed-money long position across the three U.S. wheat futures classes is historically thin and a setup for volatility — the combined long position across the 3 wheat futures classes is only 13k contracts, the largest since October 2022. The algo machines are driving, not the fundamentals crowd. Source: ADM Investor Services, March 23

3. THE HRW CROP — QUIETLY DETERIORATING BEHIND THE GEOPOLITICAL FIREWORKS:Winter wheat ratings plummeted by 22% over the last month alone, with the Brugler 500 index for Kansas dropping to a dismal 339 - The Chronical-journal. The HRW cropcondition scores due Monday are expected to deteriorate across Oklahoma,Texas and Kansas, with the Global Forecast System (GFS) and European models still at odds on meaningful rainfall beyond ten days. The southern plains drought story remains very much alive, and the forecast rains failing to materialize — as was the case throughout late February and early March — means the market is unlikely to price in weather relief until it actually arrives Today's Monday crop progress release will be closely watched. The weather is a slow-motion fundamental that could re-assert itself as the geopolitical noise dies down. Source: Grain Central, March 23

4. FERTILIZERPRICE SHOCK — THE DELAYED DETONATOR FOR 2026 CROP ECONOMICS: As of March17, 2026, DAP and MAP have risen above $700/MT [historical range: $250-$1000], urea has moved above $600/MT [historical: $194-$900], and UAN has surpassed $400/MT [historical: $390-$680]. Persian Gulf countries account for roughly 43% of seaborne urea exports, approximately 44% of seaborne sulfur trade, and more than a quarter of global ammonia exports. Unlike the disruptions experienced during the 2022 Russia–Ukraine fertilizer crisis, fertilizer produced in the Gulf cannot easily be rerouted when the Strait is closed. CAPTS This is not a futures-market problem yet — it's a spring planting cost crisisalready in motion. The Trump 5-day pause may cool energy futures, but fertilizer that isn'tin motion yet won't arrive in time for corn planting. Source: Stone

The “irregular event” is geopolitical whipsaw: grain markets had built anIran war premium into overnight trade on Monday morning, then a 4:AM Truth Social post from Trump announcing a 5-day halt on power plant strikes collapsed crude oil ~11% and drained that premium in real time. The denial that the talks happened is from a context of very high internal political pressure between Iranian hardliners and moderates. The 5-day clock runs out this coming weekend. The markets are well aware ofPresident Trump’s stick-and-carrot negotiating style and the Iranians are running out of cards to play. The underlying wheat fundamentals — deteriorating HRW crop, fertilizer price shock, strong export pace, MARS downgrade of EU yields — remain intact. This is a market in a timeout, not a trend change (yet). The Box-o-Rox exit trigger price is within a cent or two of Tuesday’s early trade. Our approach is to wait for a decisive close below that indicator line to change the status of the two (2) tranches of our new crop that have been held up during the last few weeks of uptrend. Trading any market based on “social media” is not prudent.

The trend is still upward. Stay tuned. Plan the next action.

-Gabriel

MarketBullets® — More Sense Per Bushel™

– Noticeables: <Diesel> <Gold> <US Dollar Index> <Ruble VS Yuan> <2-Yr T-Note> <S&P>

Good hunting!

See “Archived Updates” in Top Menu for historical record of commentary.

Kansas City Hard Red Winter Wheat Futures

North of Prescott, Washington

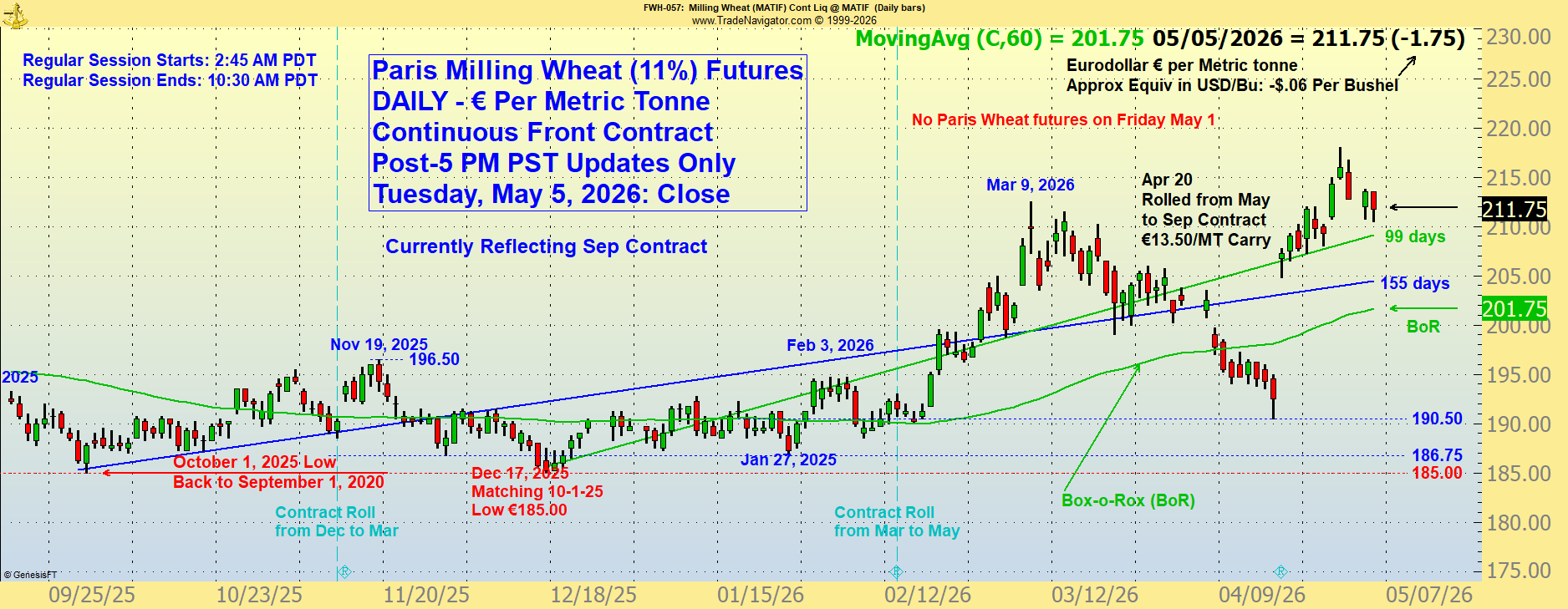

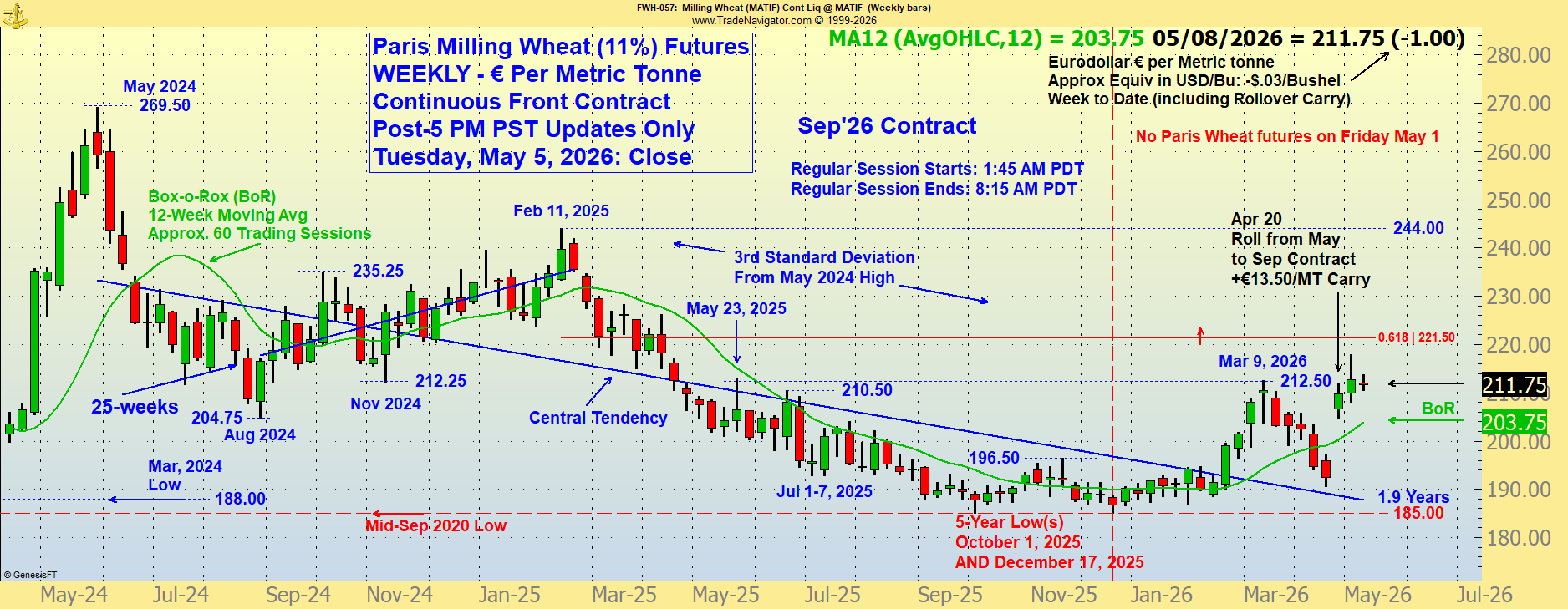

Paris Milling Wheat - Daily, Weekly and Monthly

These Charts Updated End-of-Day Only

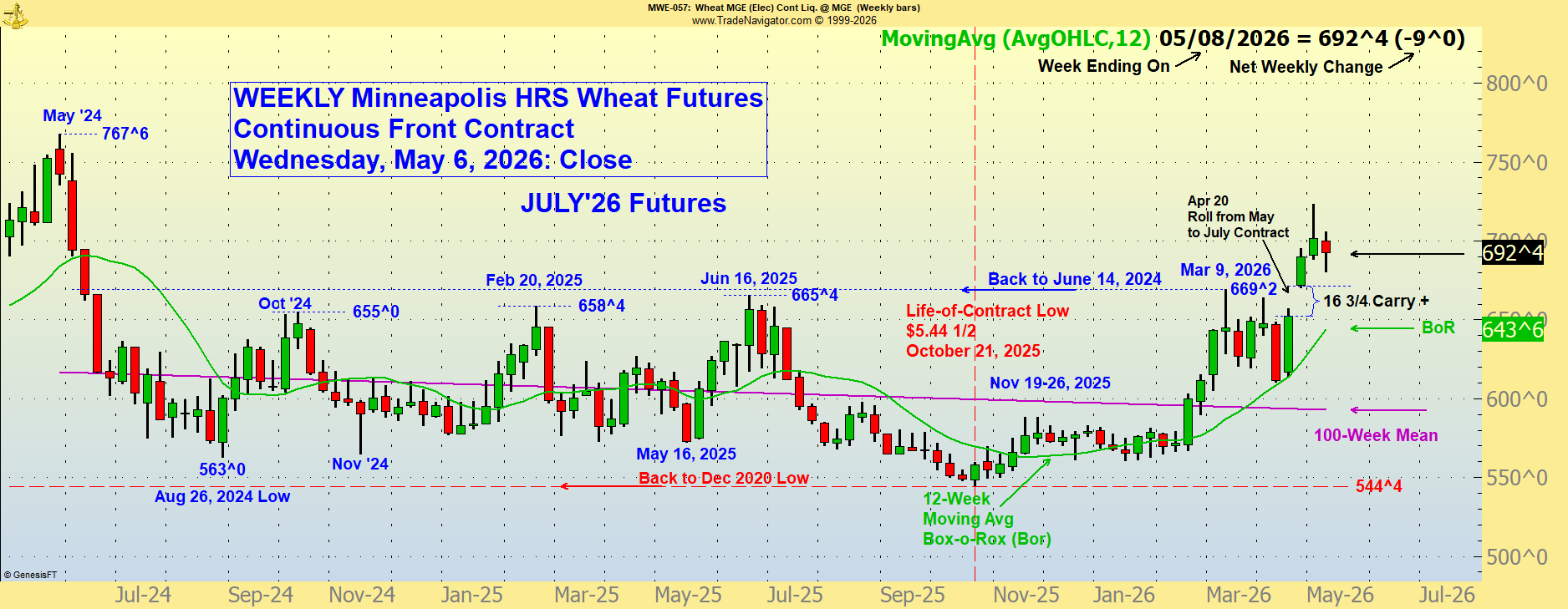

Minneapolis Hard Red Spring Futures

This Chart Updated End-of-Day Only

The Waitsburg Place

“Cultivators of the earth are the most valuable citizens. They are the most vigorous, the most independent, the most virtuous and they are tied to their country and wedded to its liberty and interests by the most lasting bands.” — Thomas Jefferson

***

Click on any of the following links:

<Paris Milling Wheat Daily> <U.S. Dollar Index Monthly> <WTI/Brent/Urals Crude>

<Diesel Daily> <Wheat Spreads> <Gold/Silver> <Nat Gas> <Interest Rates>

<Box-o-Rox (BoR)> <Commitment of Traders> <Special Info Item> <Ocean Freight Index>

<Weekly Ruble/Yuan> <Dry Bulk Ocean Freight> <Fibonacci Spiral>

RISK REMINDER: Always remember that the opinions and information on this site are intended as informative material and are believed to be drawn from reliable sources, but everything herein is subject to error and change without notice, without any guarantee as to accuracy or completeness. The management of physical grain positions and/or the use of futures, options, or other derivatives carries risks that are not appropriate for everyone, and thorough consideration of potential losses should be applied before taking or avoiding any trading action involving active markets. Any use of the content on this website is the sole responsibility of the consumer.

As of JULY 10, 2026 BoR Status Changed to: "Suspend"

See text under chart on BoR Page.

🚧 SITE UPGRADE NEARLY COMPLETE — Commentary and charts may be delayed or display errors during the transition. New version launching soon. Current BoR signals are now being updated 2x per day.

More Sense Per Bushel

Wheat Price Trends and Peripheral Markets

Charts and Comment

MARKETBULLETS®

Base (non-annotated) Charts Courtesy of Genesis Trade Navigator.

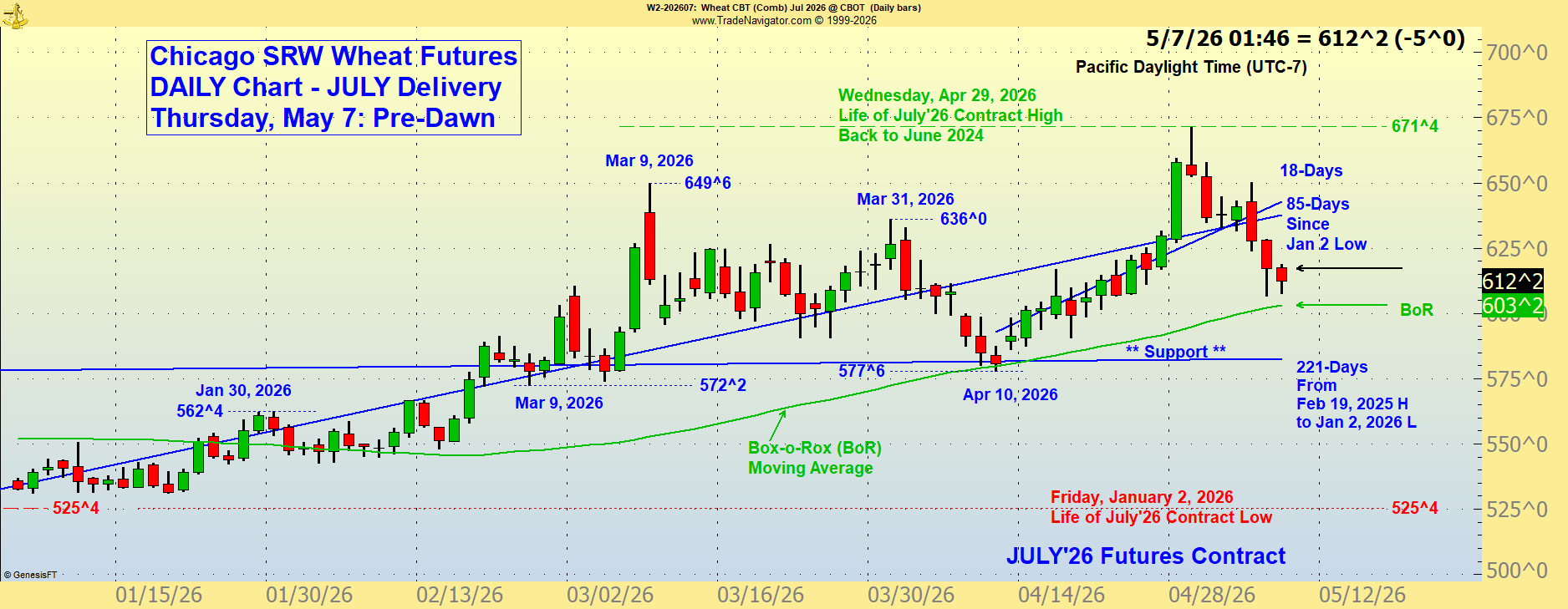

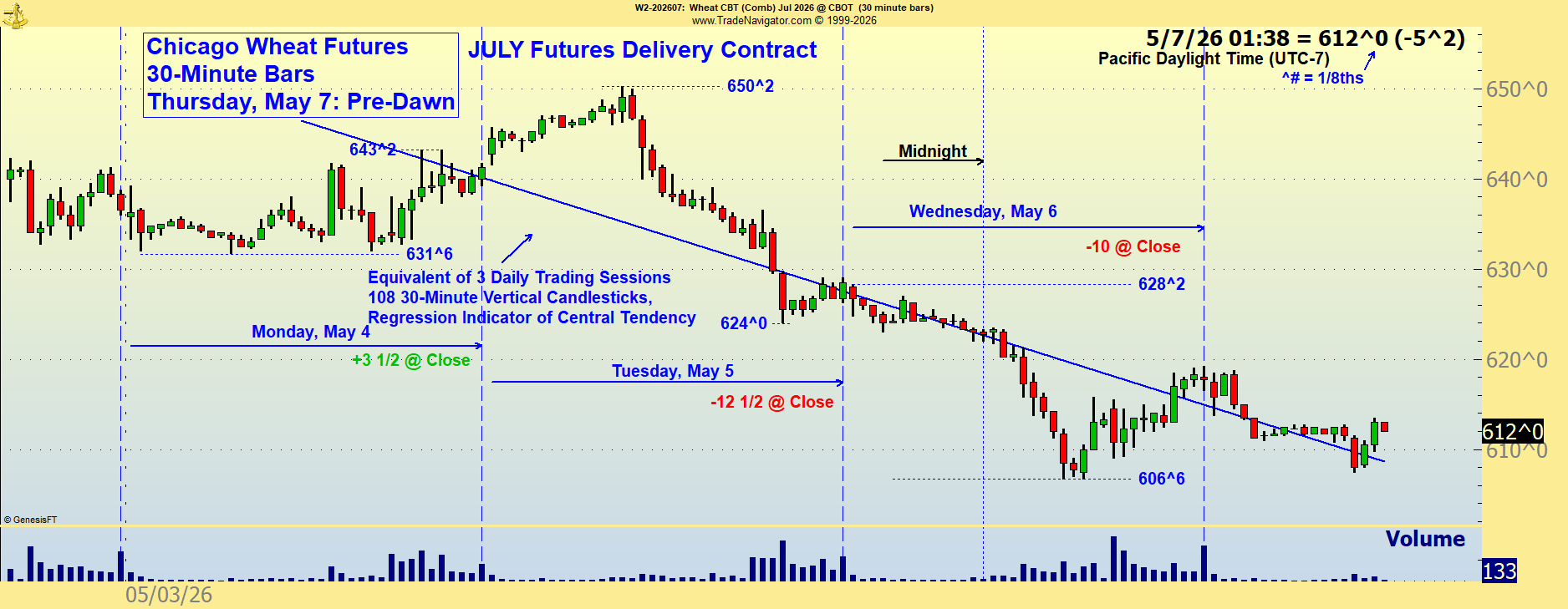

Chicago Soft Red Winter (SRW) Wheat Futures in 30-Minute Candles