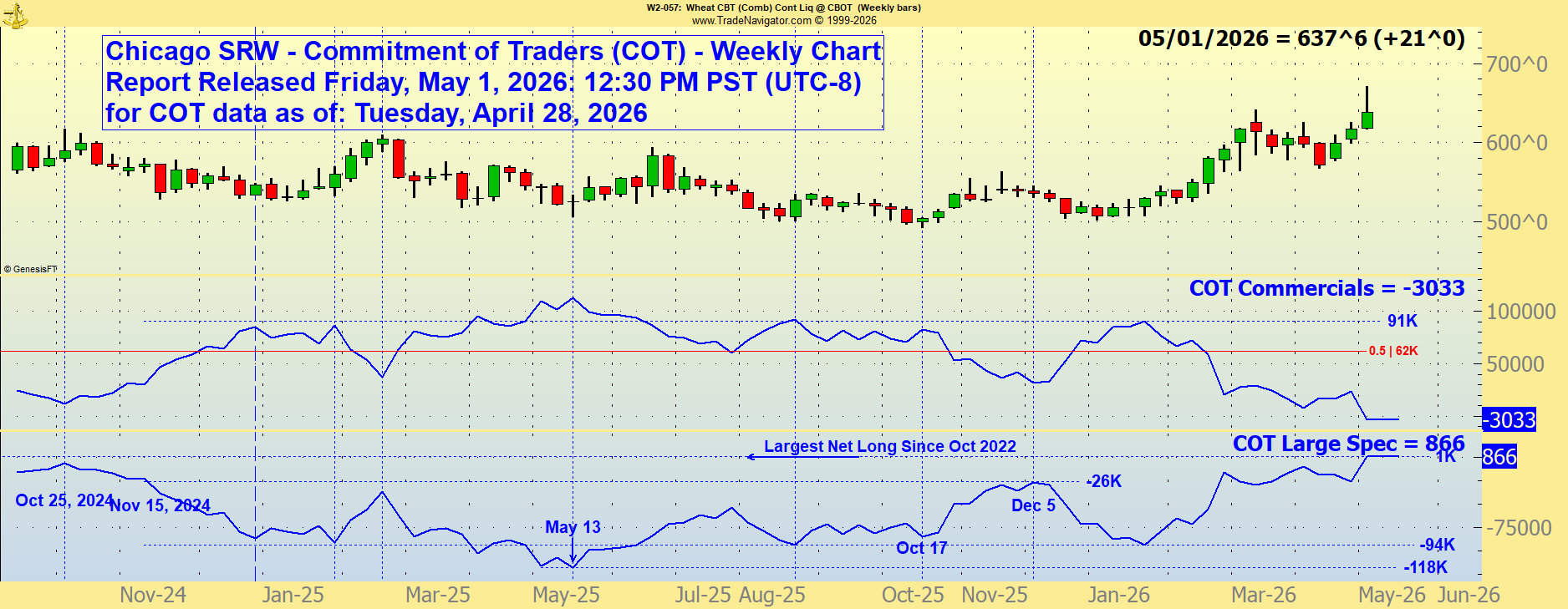

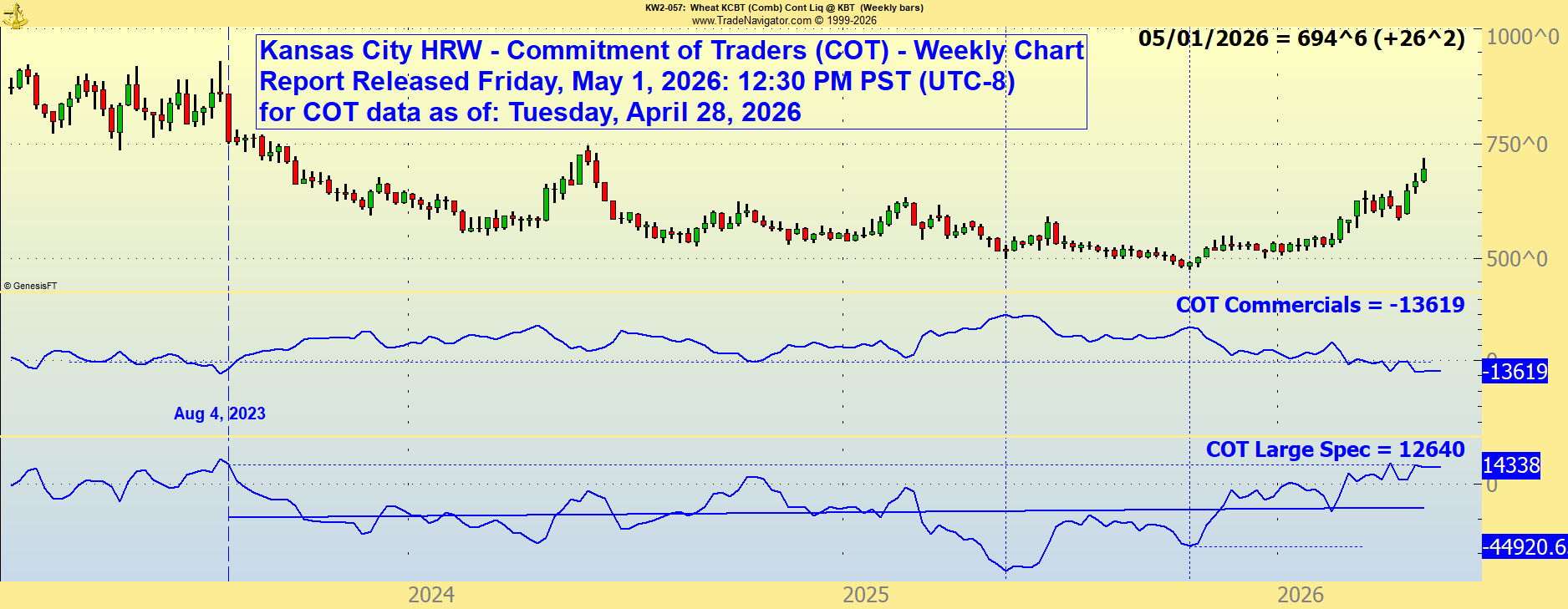

Commodity Futures Trading Commission (CFTC) Commitments of Traders (COT)

Net Positions of Commercials and Large Specs

Weekly Chart

Market Bullets® Friday, May 16, 2025: Special

Many articles about the wheat market allude to “The Money Funds”. There are large, mostly well-funded trading entities that accumulate positions in many different futures markets. Their presence has a magnitude in effect on price movements as large as the weather, or even the guvmint. They exist because they must in order for our markets to accommodate any size of business, from micro to macro. The discussion of the size and function of the futures markets, specifically the wheat markets, is well beyond the scope of this comment. At the moment the focus is on the character of these large creatures, which command so much capital in wheat.

The “Money Funds” are a feature of the futures business, categorized and monitored by the Commodity Futures Trading Commission (CFTC) in a weekly report called the “Commitment of Traders” (COT). There are several categories of trader required to report their net positions every week to the CFTC. The two most prominent of these are the “Commercials” and the “Large Speculative” accounts known as “the Funds”. The public is not given the names and direct positions of each firm, but the aggregate numbers are published every week.

The Funds are trend-followers and use every technique known to man to attempt to capitalize on the movement of wheat prices. They do not know or care about what wheat is made of unless it affects the price in some significant way. The “Commercials” are those familiar names that have been around the grain merchandizing business forever; Archer Daniels Midland (ADM), Cargill, Bunge, Ltd, Louis Dreyfus Co, and many others. Both Funds and Commercials continuously participate in the futures markets for different reasons.

The Funds always speculate. They neither own nor handle any cash grain. They care only for price movements, trading futures as a money vehicle.

The Commercials are strictly involved in handling, buying, storing, selling and otherwise providing the channel through which a vast amount of grain moves each year. Their interest in futures is to reduce their exposure to price movements. They do not speculate (much).

Awareness of the COT report is essential for any marketer of wheat. When the Funds accumulate massive net positions, it usually is the result of a long trend, during which they tend to add new positions along the way to build profit upon liquidation.

The Commercials use the market in a very predictable pattern. They buy wheat futures when they make sales commitments for later delivery to protect them from upward price movements during the time it takes to acquire and move the wheat into position for delivery. Once the cash wheat for that physical contract is acquired, they remove the futures position, as it no longer reduces risk for them. When they acquire wheat that has not already been committed to a contract for forward delivery, they sell futures to cover the risk of downward price movement until that wheat is contracted. This is a simplistic view of their participation in futures, but it is essentially what they do in those markets. They do not speculate.

When the wheat price is moving downward, the Commercials tend to accumulate less physical wheat along the way, as producers become more and more reluctant to sell. This causes them to accumulate large net-purchased “long” positions to cover obligations for forward deliveries. An extended period of downward price movement may lead to a very large net long, and the group tends very strongly to reach their largest net longs at market lows. Ironically, this means that they are always “right” about the market direction, an astonishing thing until one realizes that it has nothing to do with speculative decisions. It is the nature of their business.

Any trader can follow the positions of the Commercials and/or the Funds, but as a trading signal it may require vast amounts of capital to stay in positions like theirs, sometimes months or years. It is a very ponderous and imprecise trading indicator, but it is a great background piece of data.

Today, the Commercials are carrying historically massive wheat positions, as in +112,476 contracts as of the most recent COT report, representing 562,380,000 bushels of wheat in Chicago, and 60,103 contracts (300,515,000 bushels) in Kansas City (an all-time high). In Chicago wheat it is a larger “net long” than at any time in the past except for one brief period in 2017, preceding of a significant wheat price rally.

On the other side of the fence, we have the Big Specs, the Funds, holding a big 118,100 contracts in Chicago Soft Red Winter (SRW) and 62,689 in KC Hard Red Winter (HRW) wheat on the short-sold side. This group, when properly ignited, tends to move quickly in a herd-like pattern and can lift prices with drama, as no-one wants to be on the wrong side of a short-squeeze rally. It usually takes a hot-wire bit of news or a USDA report to light them up, but when they stampede, it can be amazing.

We can use this data, but it’s sometimes like forecasting T-storms in summer, we know the conditions that give rise to them, we can plan for them, but we cannot mark the dates in advance on the calendar. Those big clouds over the horizon, with a dropping barometer and a bit of wind…

It looks like we may have a Funds VS Commercials rally approaching, even the occasional flash of lighting on the far horizon, but no thunder and no promises yet.

Stay tuned, we will smell the storm coming.